Introduction

If you’re trying to improve your finances, you’ve probably asked yourself an important question: should you build an emergency fund first or start investing right away?

It’s a common dilemma. On one hand, investing can help your money grow and build long-term wealth. On the other hand, life is unpredictable. A medical bill, car repair, job loss, or home emergency can happen when you least expect it.

Many Americans feel pressured to start investing as soon as possible, especially when they hear stories about stock market gains. But investing without a financial safety net can create problems when unexpected expenses arise.

Understanding the difference between saving and investing is essential for making smart financial decisions. In this guide, we’ll explore the pros and cons of both strategies and help you determine which should come first based on your financial situation.

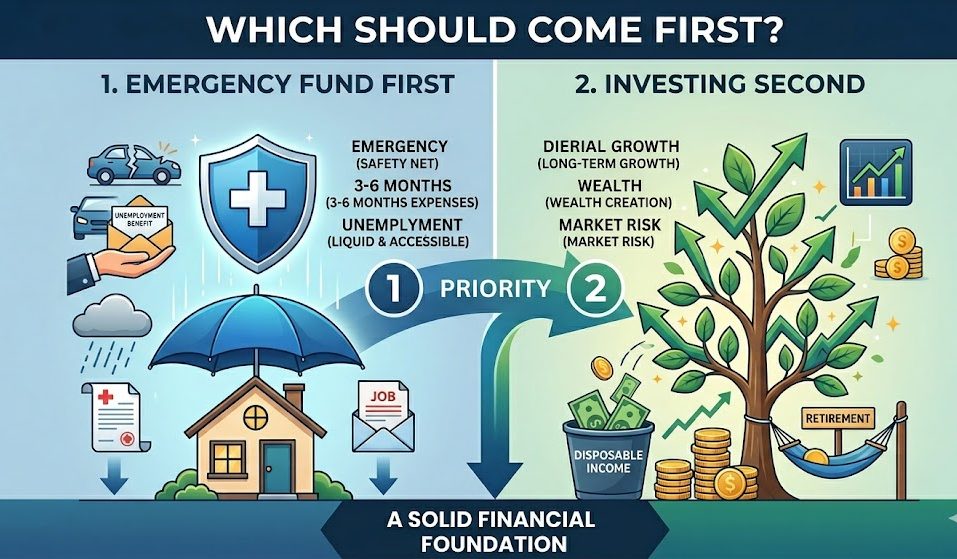

What Is an Emergency Fund?

An emergency fund is money set aside specifically for unexpected expenses.

Unlike investment accounts, emergency savings should be easily accessible when needed.

Common uses include:

- Medical emergencies

- Major car repairs

- Home repairs

- Job loss

- Unexpected travel expenses

- Family emergencies

The primary purpose of an emergency fund is to provide financial stability during difficult situations.

Think of it as a financial cushion that protects you from relying on credit cards or loans.

What Is Investing?

Investing involves putting money into assets that have the potential to grow in value over time.

Examples include:

- Stocks

- Bonds

- Index funds

- ETFs

- Real estate investments

The goal of investing is to increase your wealth over the long term.

Unlike savings accounts, investments can fluctuate in value. While they may provide higher returns, they also carry some level of risk.

Why This Decision Matters

The debate between saving and investing is important because both serve different purposes.

An emergency fund provides:

- Financial protection

- Stability

- Quick access to cash

Investing provides:

- Wealth growth potential

- Retirement preparation

- Long-term financial opportunities

The challenge is finding the right balance between the two.

The Risks of Investing Without an Emergency Fund

Many beginners focus entirely on investing because they want their money to grow.

However, investing before establishing emergency savings can create problems.

Imagine this situation:

You invest $5,000 in the stock market.

A few months later:

- Your car transmission fails.

- Repair cost: $3,000.

If you don’t have emergency savings, you may need to:

- Sell investments

- Use credit cards

- Take out loans

If the market happens to be down at that time, you could be forced to sell investments at a loss.

This is one of the main reasons financial experts often recommend building emergency savings first.

Benefits of Having an Emergency Fund

A strong emergency fund offers several advantages.

Financial Security

Unexpected expenses become easier to manage.

Reduced Stress

Knowing you have savings available can provide peace of mind.

Less Debt

Emergency savings can help prevent reliance on high-interest credit cards.

Flexibility During Job Loss

An emergency fund can help cover living expenses while searching for new employment.

Benefits of Investing Early

Although emergency savings are important, investing also offers significant advantages.

Compound Growth

One of the biggest benefits of investing is compound growth.

When investments earn returns, future returns may be generated on both the original investment and previous gains.

Over time, this effect can significantly increase wealth.

Long-Term Wealth Building

Investing helps support goals such as:

- Retirement

- Home ownership

- Education funding

- Financial independence

Protection Against Inflation

Money sitting in low-interest accounts may lose purchasing power over time due to inflation.

Investments can potentially help offset this effect.

Real-Life Example: A Balanced Approach

Consider David, a 29-year-old software developer in Texas.

David wanted to start investing but had almost no savings.

Instead of putting all his extra money into the stock market, he created a plan:

- First, he built a small emergency fund.

- Then, he began investing modest amounts.

- He continued growing both savings and investments over time.

Within two years, he had:

- Emergency savings for unexpected expenses

- A growing investment portfolio

- Greater financial confidence

His balanced approach helped him avoid unnecessary financial risk.

How Much Should Be in an Emergency Fund?

Financial experts often recommend saving enough to cover several months of essential living expenses.

This may include:

- Rent or mortgage payments

- Utilities

- Groceries

- Insurance

- Transportation costs

The exact amount depends on factors such as:

- Income stability

- Family size

- Employment situation

- Monthly expenses

People with variable income may choose larger emergency funds.

A Step-by-Step Strategy for Beginners

If you’re unsure whether to save or invest first, consider this practical approach.

Step 1: Build a Starter Emergency Fund

Aim for a small financial cushion first.

Even a modest emergency fund can help cover unexpected expenses.

Step 2: Pay Down High-Interest Debt

High-interest debt can make wealth building more difficult.

Reducing expensive debt often provides a strong financial foundation.

Step 3: Begin Investing Consistently

Once basic savings are established, start investing regularly.

Focus on long-term goals rather than short-term market movements.

Step 4: Continue Growing Emergency Savings

Keep building your emergency fund until it reaches your desired level.

Step 5: Increase Investments Over Time

As income grows, increase investment contributions when possible.

Common Mistakes to Avoid

Many people make avoidable financial mistakes.

Investing Money Needed Soon

Short-term funds generally should not be invested in volatile assets.

Ignoring Emergency Savings

Unexpected expenses happen to everyone.

Keeping Excessive Cash

While emergency savings are important, keeping all money in cash may limit long-term growth opportunities.

Trying to Time the Market

Consistently predicting market highs and lows is extremely difficult.

Neglecting Financial Goals

Your strategy should align with your personal objectives.

Finding the Right Balance

The question isn’t always emergency fund versus investing.

For many Americans, the best solution involves both.

A balanced approach often looks like this:

- Build emergency savings

- Invest regularly

- Reduce debt

- Increase contributions over time

This strategy helps create both short-term security and long-term wealth.

Frequently Asked Questions (FAQ)

1. Should I save or invest first?

Many financial professionals recommend building at least a basic emergency fund before focusing heavily on investing.

2. How much should I keep in emergency savings?

The amount varies depending on your financial situation, expenses, and income stability.

3. Can I save and invest at the same time?

Yes. Many people split their extra money between savings and investments.

4. Where should I keep my emergency fund?

Emergency savings are often kept in accounts that provide easy access to funds when needed.

5. Is investing risky?

All investments carry risk, but diversification and long-term planning can help manage that risk.

6. What is the biggest advantage of investing early?

Starting early allows more time for compound growth to work in your favor.

Conclusion

The debate between emergency savings and investing doesn’t have a one-size-fits-all answer. However, for most Americans, building a basic emergency fund before making major investments is often a smart financial move.

Emergency savings provide protection against life’s unexpected challenges, while investing helps build long-term wealth and financial independence. Rather than viewing them as competing goals, think of them as two important parts of a strong financial foundation.

By creating a balanced strategy that prioritizes both security and growth, you can protect yourself today while working toward a more prosperous future.

Financial success isn’t about choosing one over the other—it’s about knowing when and how to use both effectively.

Call to Action (CTA): Encourage readers to explore more articles on the website.

Want more practical personal finance tips? Explore more articles on our website for expert advice on saving money, investing wisely, managing debt, building wealth, and achieving long-term financial success.