Introduction

Graduating from college is a major achievement. After years of studying, attending classes, and working toward a degree, many students look forward to starting their careers and building their future. However, for millions of Americans, graduation also brings a new responsibility: managing student loan debt.

Receiving that first loan statement can feel overwhelming. Questions about monthly payments, interest charges, and long-term financial goals often begin to surface. Many graduates worry about how student loan payments will fit into their budget while also paying for housing, transportation, insurance, and daily living expenses.

The good news is that student loan debt doesn’t have to control your financial future. With the right strategies, careful planning, and consistent habits, graduates can successfully manage their loans while working toward other financial goals.

This guide provides practical tips for managing student loan debt after graduation, helping borrowers stay organized, reduce financial stress, and build a stronger financial foundation.

Why Managing Student Loan Debt Matters

Student loans can affect many areas of your financial life.

These may include:

- Monthly budgeting

- Saving money

- Building credit

- Buying a home

- Investing for retirement

- Achieving financial independence

Ignoring student loans can lead to financial challenges, while managing them responsibly can help create long-term stability.

The sooner graduates develop a repayment strategy, the easier it becomes to stay on track.

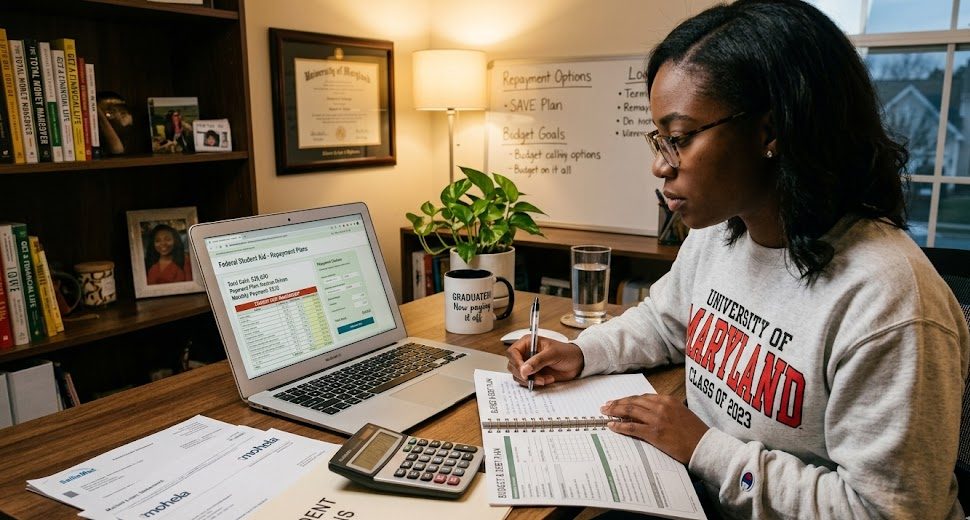

Understand Exactly What You Owe

One of the first steps after graduation is understanding your student loan situation.

Review:

- Total loan balance

- Interest rates

- Monthly payment amounts

- Repayment schedule

- Loan servicer information

Many graduates have multiple loans and aren’t fully aware of their total debt.

Creating a complete picture of your student loan obligations helps you make informed financial decisions.

Create a Realistic Monthly Budget

A budget is one of the most powerful tools for managing debt.

Without a budget, it’s easy to overspend and struggle with monthly payments.

Your budget should include:

Essential Expenses

- Rent or mortgage

- Utilities

- Transportation

- Groceries

- Insurance

Debt Payments

- Student loans

- Credit cards

- Other financial obligations

Savings

- Emergency fund contributions

- Long-term financial goals

A clear budget allows you to prioritize student loan payments without neglecting other important financial needs.

Make Payments on Time

One of the most important tips for managing student loan debt after graduation is making every payment on time.

Consistent payments can help:

- Avoid late fees

- Maintain good standing

- Build a positive credit history

- Reduce financial stress

Even a few missed payments can create unnecessary complications.

Setting up automatic payments can help ensure deadlines are never overlooked.

Build an Emergency Fund

Unexpected expenses happen to everyone.

Examples include:

- Car repairs

- Medical bills

- Job loss

- Emergency travel

Without savings, many borrowers rely on credit cards when emergencies arise.

Building an emergency fund creates a financial safety net and helps prevent additional debt.

Even small, regular contributions can grow over time.

Understand Your Repayment Options

Not every repayment plan works for every borrower.

Depending on your situation, there may be multiple repayment options available.

Factors to consider include:

- Income level

- Career stage

- Family responsibilities

- Financial goals

Understanding available repayment plans can help you find an approach that fits your budget.

Pay More Than the Minimum When Possible

Making minimum payments keeps your account current, but paying extra may offer additional benefits.

Potential advantages include:

- Faster debt reduction

- Lower total interest costs

- Greater financial flexibility

Even small additional payments can make a meaningful difference over time.

The key is consistency rather than large occasional payments.

Real-Life Example: A Smart Repayment Strategy

Consider Jason, a recent graduate from Illinois.

After earning his degree, he started working in a marketing position.

Instead of ignoring his student loans, he created a plan:

- Developed a monthly budget

- Built a small emergency fund

- Set up automatic payments

- Applied extra money toward loan balances when possible

Within a few years, Jason significantly reduced his debt while maintaining healthy financial habits.

His success came from consistency rather than drastic financial sacrifices.

Avoid Lifestyle Inflation

One common mistake new graduates make is increasing spending too quickly after securing their first full-time job.

It’s tempting to spend more on:

- New vehicles

- Luxury apartments

- Expensive vacations

- High-end electronics

While enjoying the rewards of hard work is important, excessive spending can make student loan repayment more difficult.

Maintaining a balanced lifestyle can help accelerate financial progress.

Monitor Interest Costs

Interest plays a major role in student loan repayment.

The longer a balance remains unpaid, the more interest may accumulate.

Understanding interest helps borrowers:

- Prioritize repayment

- Evaluate financial decisions

- Identify opportunities to save money

Paying attention to interest costs can improve long-term financial outcomes.

Consider Refinancing Carefully

Some borrowers explore refinancing options to potentially obtain different loan terms.

Potential benefits may include:

- Simplified payments

- Different repayment structures

- Potential interest savings

However, refinancing decisions should be evaluated carefully based on individual circumstances.

Understanding the potential advantages and trade-offs is essential before making changes.

Step-by-Step Plan for Managing Student Loan Debt

If you’re feeling overwhelmed, follow this practical roadmap.

Step 1: Organize Loan Information

Gather details about all student loans.

Step 2: Create a Budget

Allocate income toward essential expenses and debt payments.

Step 3: Build Emergency Savings

Establish a financial cushion for unexpected expenses.

Step 4: Automate Payments

Reduce the risk of missed deadlines.

Step 5: Pay Extra When Possible

Apply additional funds toward loan balances.

Step 6: Review Progress Regularly

Track repayment milestones and adjust your strategy as needed.

Common Mistakes to Avoid

Many graduates unintentionally make repayment harder.

Ignoring Loan Statements

Stay informed about balances and payment schedules.

Missing Payments

Late payments can create financial and credit challenges.

Living Beyond Your Means

Excessive spending can delay financial progress.

Neglecting Savings

Emergency savings remain important even while paying debt.

Failing to Understand Loan Terms

Knowledge helps borrowers make smarter decisions.

Benefits of Effective Student Loan Management

Responsible repayment offers several advantages.

Reduced Financial Stress

A clear plan creates confidence.

Better Credit Health

Consistent payments support positive credit history.

Faster Debt Freedom

Strategic repayment helps reduce balances more quickly.

Improved Financial Opportunities

Less debt may make it easier to pursue future goals such as:

- Homeownership

- Investing

- Retirement planning

- Starting a business

Frequently Asked Questions (FAQ)

1. What is the best way to manage student loan debt after graduation?

Creating a budget, making on-time payments, and building emergency savings are among the most effective strategies.

2. Should I pay more than the minimum payment?

Extra payments may help reduce interest costs and shorten the repayment timeline.

3. Why is an emergency fund important while repaying loans?

Emergency savings can help prevent new debt when unexpected expenses arise.

4. How does student loan repayment affect credit?

Consistent on-time payments can support a positive credit history.

5. Can budgeting really help with student loan repayment?

Yes. A budget helps ensure income is allocated efficiently and payments remain manageable.

6. How often should I review my repayment strategy?

Reviewing your finances at least once or twice a year can help keep your plan aligned with your goals.

Conclusion

Managing student loans after graduation may seem challenging at first, but it becomes much easier with a clear plan and consistent financial habits. By understanding your loan details, creating a realistic budget, building emergency savings, and making timely payments, you can take control of your debt rather than letting it control you.

These tips for managing student loan debt after graduation are designed to help borrowers build confidence, reduce stress, and make steady progress toward financial freedom. Remember that successful repayment isn’t about perfection—it’s about making smart decisions consistently over time.

Every payment moves you closer to your goals, and every positive financial habit strengthens your future. With patience, discipline, and the right strategy, student loan debt can become a manageable part of your financial journey rather than a lifelong burden.

Call to Action (CTA): Encourage readers to explore more articles on the website.

Looking for more expert advice on student loans, personal finance, budgeting, investing, insurance, and wealth-building strategies? Explore more articles on our website for practical tips that can help you make smarter financial decisions and achieve long-term financial success.